A few basics on credit cards:

- All credit cards give you a certain time to pay for the purchases you have made – therefore giving you credit – This is your “Grace Period.”

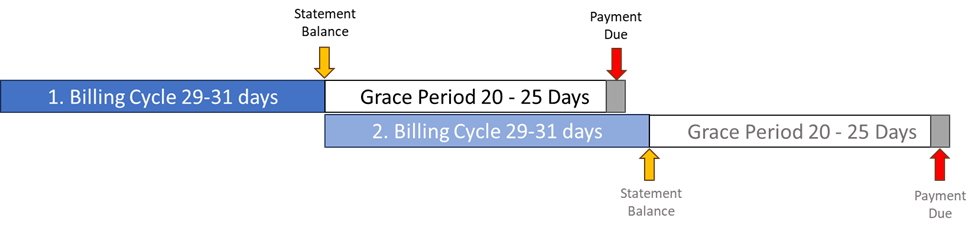

- The billing cycle is usually 29 to 31 days, and the last date of your billing cycle is your Statement closing date.

- The payment due date is usually 20- 25 days from the Statement Date, giving you time to pay the balance from your last billing cycle. Some companies give you certain dates in the month to choose. It can be helpful to choose the Payment date that is furthest from your Statement date

- Notice how none of the dates match. If you choose a specific payment date every month, such as the 6th or 21st, the number of days you must pay your Statement balance will also fluctuate.

- A minimum payment amount can be set up to avoid being late, but keep in mind, that by not paying off more, you’ll also pay more interest.

If you only pay the Minimum payment amount of 2 - 3% of the statement balance, it will take 20 years or more to pay off. - The most profitable customers for credit card companies are those who pay the minimum amount and carry their balance over every month.

A few tips to avoid never-ending credit card payments.

- Always pay more than the minimum payment amount. If the minimum payment amount is less than 3% of your statement balance and the interest rate is 29.99%, you could be paying the interest only, forever!

- A starter credit card with a $500 credit limit, a $100 annual Fee, and 29.99% APR when paying a minimum amount for a year will cost you $250 plus any other fees they may charge. You just paid $250 to borrow $500 for a year!

You can find more details on all the terms and definitions on a typical credit card statement below.

Interactive Credit Card Statement

https://mycreditunion.gov/life-events/checking-credit-cards/credit-cards/statement

https://credit.org/blog/how-to-read-your-credit-card-statement/

Comments